Our country entered a recalibration phase in the second month of the first quarter, in which the Government tried to combine fiscal consolidation with economic recovery measures, in a context marked by budgetary pressures, high inflation and slowing growth. Fiscal package number 3, announced by the Government in February, had a double goal: on the one hand, stimulating investments and unblocking liquidity in the economy, and on the other hand, strengthening collection discipline, in an effort to regain control over public finances and investor confidence.

The economic recovery component was built around concrete incentives for the business environment: bonuses for timely payment of taxes, the expansion of the VAT collection system to reduce the pressure on companies' cash flow, facilities for micro-enterprises and tax measures dedicated to investments, such as the tax credit for research and development and accelerated depreciation. In parallel, incentives for the capital market were also introduced, in an attempt to direct domestic saving towards financing the real economy. This mix indicates a change in approach, in which the state tries to support private capital, but without giving up fiscal control instruments. An important signal of stability came from the domestic financing market, where the FIDELIS program attracted over 1.013 billion lei in just a few days, through over 12,000 subscription orders. The high interest in government bonds, including long-term ones, shows that the population remains an essential pillar in financing the deficit, offering the state a viable alternative to foreign markets, at a sensitive time.

On the budgetary front, the execution for February 2026 confirmed that the measures adopted by the Bologna government last year are yielding the expected results: the budget deficit dropped to 14.23 billion lei, equivalent to 0.70% of GDP, half the level of last year when it was 30.24 billion lei in the first two months, respectively 1.58% of GDP. At the same time, at the end of February 2026, a 15.7% increase was recorded, compared to the first two months of 2025, in total revenues, which reached 103.73 billion lei, while expenditures were 117.96 billion lei, nominally decreasing by 1.6% and reducing as a share in GDP from 6.3% to 5.8%, compared to February 2025.

In this context, monetary policy remained strict. The Board of Directors of the National Bank of Romania decided, on February 17, to maintain the key interest rate at 6.5%, signaling that the fight against inflation is far from over. Especially since, subsequently, according to data presented by the National Institute of Statistics, the annual inflation rate fell only marginally, to 9.31% in February, which confirms the persistence of inflationary pressures and limits the space for monetary easing.

Overall, February 2026 outlines an economy in a delicate balance: the state is trying to stimulate investment and restart growth mechanisms, while maintaining stricter fiscal discipline and a prudent monetary policy. The results indicate first signs of stabilization, but also the fact that the economic recovery remains dependent on maintaining this balance in a context still marked by internal and external uncertainties. Unfortunately, February, although it also marked the beginning of the first parliamentary session of 2026, ended without the Government adopting the draft state budget law and the draft state social insurance budget law for the current year, postponing this obligation to March.

• Economic recovery package, the governing coalition's priority in February

The government built, in February 2026, a fiscal package, followed by one on economic recovery, through which it tries to reset the relationship with taxpayers, stimulate real investments and reduce chronic liquidity bottlenecks in the economy, but without giving up strict control over collection and budgetary discipline.

One of the most visible measures was the introduction of a 3% bonus on the tax due for the fiscal year 2025, applicable to both companies - corporate tax payers or micro-enterprises - and individuals who file the Single Declaration. It is, in practice, the first explicit attempt to reward correct fiscal behavior, not just to sanction deviation. The condition is firm, however: full and timely payment, by April 15, 2026, which transforms this facility into a pressure tool to increase collection in the short term.

At the same time, the Government intervened directly on one of the biggest problems of the business environment, the liquidity bottleneck generated by VAT. The ceiling for the VAT on receipt system is increased to 5 million lei in 2026 and to 5.5 million lei from 2027, which allows a significantly larger number of companies to pay VAT only after they actually collect their invoices. In real terms, this means a reduction in the forced financing of the state by companies and an immediate release of cash flow, in a tense economic context.

For micro-enterprises, fiscal package number 3 is one of clear flexibility, but also of correction of some rigidities that have generated artificial exits from the system. The deadline for hiring the first employee increases to 90 days for new companies, and income from the occasional sale of assets is no longer included in the 100,000 euro ceiling, thus avoiding the modernization penalty. In addition, the sick leave of the sole employee no longer automatically leads to the loss of the tax regime, which eliminates an absurd vulnerability for small businesses.

A change with an immediate impact on companies' accounting is the increase in the threshold for fixed assets from 2,500 lei to 5,000 lei, which allows the direct deduction, as an expense, of a larger volume of purchases. It is an apparently minor measure, but it reduces bureaucracy and accelerates the tax recovery of small investments.

In the area of investments, the Government introduces a 10% tax credit for research and development, deductible from tax, but also the possibility of accelerated depreciation - up to 65% of the asset value in the first year - for equipment purchased in 2026. The combination of these two instruments creates a significant tax advantage for companies that invest quickly in technology, in a year in which the state is trying to force modernization.

In parallel, direct incentives are being introduced for the capital market: an additional deduction of 50% for the costs of listing on the stock exchange and deductions of up to 400 euros annually for individuals who invest in shares, bonds or ETFs. It is an obvious attempt to shift part of the population's savings towards financing the real economy.

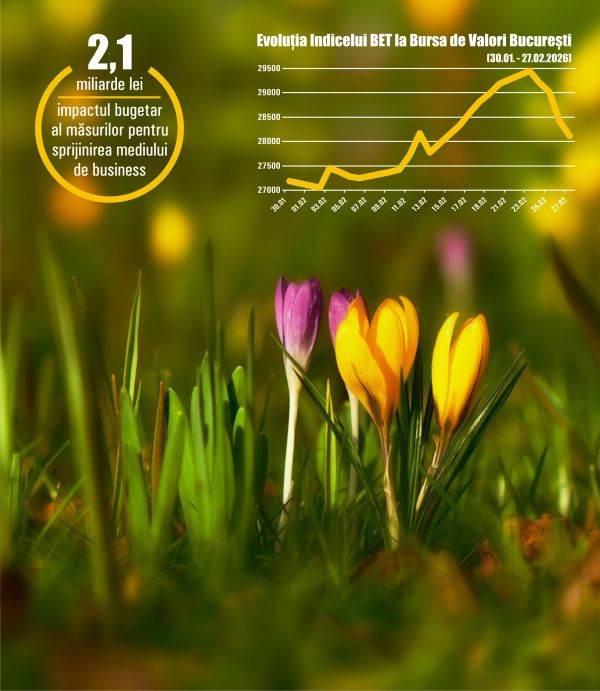

According to the adopted legislation, the budgetary impact in 2026 amounts to 2.1 billion lei, but the Government representatives claim that investing that amount in the national economy will return to the state budget, through taxes and duties, total revenues much higher than those foreseen for the economic recovery in the following years.

But the fiscal package is not just about incentives. The Government is also introducing tough disciplinary and collection mechanisms: automatic exchange of tax data between authorities, conditioning property transfers on the payment of taxes, expanding sanctions for local authorities that do not control construction and even suspending driving licenses for non-payment of fines, at a rate of one day of suspension for every 50 lei owed.

We note that the 3rd fiscal package, which also includes the economic recovery, was adopted by the Government, after the Constitutional Court of Romania rejected on February 18 the objections raised by the High Court of Cassation and Justice regarding the law on special pensions for magistrates. The CCR considered that the respective normative act complies with the provisions of the Constitution, thus creating the fiscal space necessary for the Executive to continue the reforms started last year.

• Fitch reconfirms our country rating

The credibility of the measures taken by the Government received positive feedback from Fitch Ratings, which last month reconfirmed Romania's sovereign rating at BBB-, with a negative outlook. The agency explicitly acknowledges that the fiscal consolidation measures, including the VAT increase from 2025 and the freeze on public spending in 2026, have started to produce effects, pushing the deficit on a downward trajectory, with an estimated correction of almost 2 percentage points this year. At the same time, financing costs have fallen significantly, from over 7.4% to around 6.5%, a sign that investors still give Romania a vote of confidence, albeit a cautious one. But the picture is not without risks: economic growth is estimated to be below 2% by 2027, and public debt, already close to 59% of GDP at the end of 2025, could rise to 63% if the pace of adjustments is not maintained. Fitch's message is unequivocal: Romania has avoided downgrading, but remains under pressure, and every fiscal decision matters. In this context, last month, Prime Minister Ilie Bolojan met with representatives of the Moody's rating agency, at Victoria Palace, whom he assured that our country remains on the path of fiscal consolidation, despite a large package of economic incentives that, at least in the short term, will reduce budget revenues. The 6.2% deficit target for the end of 2026 was reaffirmed as a firm commitment, as the Executive simultaneously tries to maintain a high level of investment, especially through completion of projects in the PNRR by August 31, 2026. In front of Moody's, the Prime Minister emphasized three essential directions: controlling public spending, increasing collection and stimulating investments. Basically, the Government is trying to convey that we are not witnessing uncontrolled fiscal relaxation, but a recalibration of the economic model, in which incentives for investment are offset by administrative reforms and stricter budgetary discipline. The reduction of personnel expenses in the administration, the restructuring of the public apparatus and the digitalization of ANAF were presented as guarantees that the deficit will not get out of control.

• The state continues to borrow from the population

In parallel, the Ministry of Finance continued to secure its internal financing, and the February edition of the FIDELIS program shows a consistent appetite of the population for government bonds. Over 1.013 billion lei were attracted in just a few days, through 12,103 subscription orders, in a mix of investments in lei and euros, reflecting both the need for yield and the desire for safety. The strong interest in long maturities, especially the 10-year euro, which attracted the equivalent of approximately 436 million lei, indicates an essential element: despite macroeconomic tensions, investors - including small ones - are willing to tie their savings to the Romanian state for the long term. It is a rare signal of stability in an environment dominated by uncertainty, and the fact that the FIDELIS program has reached almost 65 billion lei in total attracted confirms that the state has found an efficient channel of direct financing, reducing dependence on foreign markets.

The execution of the general consolidated budget in the first two months of 2026 indicates a significant correction of fiscal imbalances, with the deficit dropping to 14.23 billion lei, equivalent to 0.70% of GDP, half the level of 30.24 billion lei, respectively 1.58% of GDP, recorded in the same period last year, which marks a 0.88 percentage point reduction in the deficit as a share of the economy, in the context of solid revenue dynamics and a moderation in expenditures. Total revenues reached 103.73 billion lei, up 15.7% compared to the first two months of 2025, an advance supported mainly by current revenues, while expenditures were 117.96 billion lei, down 1.6% nominally and decreasing as a share in GDP from 6.3% to 5.8%, given that social assistance expenditures increased marginally, by 0.9%, to 43.18 billion lei, influenced also by fiscal-budgetary measures and payments for energy bill compensation, which amounted to 6.97 million lei in the analyzed period. Interest expenses remained at 10.26 billion lei, at a similar level to the previous year, while personnel expenses decreased to 27.13 billion lei, almost one billion lei less than the same period in 2025, as a result of the reduction of some bonuses and measures to limit wage expenses, also dropping as a share in GDP to 1.3%. Expenditure on goods and services was 14.43 billion lei, down 2.1%, while investment expenses reached 11.20 billion lei, the majority of which, respectively 76.82%, representing payments for projects financed from non-reimbursable external funds, including from the 2021-2027 financial framework and the National Recovery and Resilience Plan, both on the grant and loan components.

• BNR maintains reference interest rate, with inflation at 9.31%

In this tense financial-fiscal context, the National Bank of Romania decided to maintain monetary policy, while inflation has only marginally decreased, a sign that pressures in the economy remain strong, persistent and difficult to tame. The key decision of the month came on February 17, when the BNR Board of Directors decided to maintain the monetary policy interest rate at 6.50% per annum, to keep the Lombard lending facility rate at 7.50% and the deposit facility rate at 5.50%, as well as to keep the minimum reserve requirements for lei and foreign currency liabilities of credit institutions unchanged. In other words, the central bank chose continuity and prudence, at a time when the economy does not yet offer room for experiments. The NBR based its decision on a complicated picture, in which inflation began to decline, but too slowly to allow for real optimism. In December 2025, the annual inflation rate reached 9.69%, compared to 9.88% in September, and in January 2026 it decreased only marginally, to 9.62%. February followed, when data published by the National Institute of Statistics showed another slight reduction, to 9.31%. The structure of inflation in February is worrying. Services led the wave of price increases by far, with an annual advance of 11.37%, confirming that the strongest pressures are increasingly shifting to the domestic area of the economy, where wage costs, inflationary expectations and price rigidities are the most difficult to correct. Non-food goods rose by 9.41%, and food by 7.89%, which shows that price increases remain generalized and continue to erode purchasing power. In monthly terms, the consumer price index in February, compared to January, was 100.59%, and the cumulative inflation since the beginning of the year, reported to December 2025, reached 1.5%. Moreover, the average rate of price increase in the last 12 months, for the period March 2025 - February 2026, compared to the previous 12 months, was 8.1%, clear evidence that inflation is not just a cyclical episode, but a phenomenon with depth and inertia.

The European HICP indicator offers the same conclusion: price increases remain too high for the comfort of a central bank. In February 2026, the Harmonized Index of Consumer Prices increased by 0.57% compared to January, and the annual rate, calculated on the basis of this indicator, was 8.3%, while the average price increase in the last 12 months was 7.3%. Even if these figures are below the dynamics of the CPI, they confirm that Romania remains in a high inflation area, incompatible with a rapid relaxation of monetary policy. More worrying for the NBR is the fact that core inflation remains stubbornly high. The adjusted CORE2 annual inflation rate rose to 8.5% in December 2025, from 8.1% in September, and remained at 8.5% in January 2026. This is perhaps the clearest evidence that the problem is no longer just one of exogenous shocks or administered prices, but one deeply rooted in the internal mechanisms of the economy: still high wage costs, persistent inflationary expectations, indirect effects of the increase in the price of electricity, plus influences from the increase in the prices of some agri-food commodities and the leu/euro exchange rate. In other words, even if certain volatile components slow down, the hard core of inflation continues to put pressure and force the central bank to be extremely vigilant. In this context, the NBR forecast for the end of 2026 was revised upwards to 3.9%, compared to the previous 3.7%, which says everything about the difficulty of returning to normal. For the end of 2027, the central bank anticipates an annual inflation rate of 2.8%, within the long-term target range. It is an optimistic outlook, but conditioned by an essential variable: fiscal discipline and the avoidance of new administrative or energy shocks.

Against this background, the monetary and financial picture in February is revealing. The non-governmental credit balance increased by 0.6% compared to January, to 449.017 billion lei, but, in real terms, it stagnated, a sign that inflation continues to grind down the nominal advance. Compared to February 2025, non-governmental credit increased by 6.8%, but, in real terms, it decreased by 2.3%. Lei-denominated credit, which accounts for 67.8% of the total, advanced by only 0.3% compared to the previous month and by 3.7% compared to the same period last year, but recorded a real decline of 5.2%. In contrast, foreign currency credit grew more quickly, by 1.2% month-on-month and by 14.2% annually, equivalent to 11.6% if expressed in euros. This detail is essential: an increasingly important part of the financing dynamics is moving towards the foreign currency component, which may introduce additional vulnerabilities in an economy that must remain attentive to the exchange rate and external financing costs.

Even more telling is the evolution of deposits. Deposits of non-governmental resident clients increased in February by 0.7%, to 668.718 billion lei, and compared to February 2025 they advanced by 6.7%, but remained in the red in real terms, by 2.4%. Household deposits in lei rose by 1.4% compared to January and by 6.7% compared to the same month in 2025, but still with a real loss of 2.4%. This means that, despite an apparent increase in savings, the money set aside by the population continues to lose ground to price increases. Household deposits in foreign currency remained practically unchanged compared to January, but increased by 11.7% in lei and by 9.1% in euros compared to February 2025, confirming a trend of partial refuge in foreign currency-denominated assets. This is a subtle but important signal about the cautious confidence of the population and about the way inflation and uncertainty are repositioning the financial behavior of residents.

This picture is directly related to the data published by the NBR on February 16 on the current account and external debt. In the period January-December 2025, the current account deficit reached 30.127 billion euros, compared to 28.853 billion euros in 2024. In the same period, direct investments by non-residents in Romania rose to 8.153 billion euros, from 5.602 billion euros, which represents a positive sign, but not enough to erase concerns about external imbalances. Even more pressing is the total external debt, which increased by 23.837 billion euros, to 227.347 billion euros. Long-term external debt reached 179.431 billion euros, representing 78.9% of the total, and short-term debt stood at 47.916 billion euros. Even though the coverage of short-term external debt with foreign exchange reserves rose to 104.8%, and the coverage of imports of goods and services increased to 6 months, the overall picture remains that of an economy still living under the burden of structural imbalances.

• Government acquires Giurgiulesti port in the Republic of Moldova

Last month, the Government announced that the operator ICS Danube Logistics, which managed the Giurgiulesti port in the Republic of Moldova, had been taken over by the National Company Administration of Maritime Ports Constanta. We note that the Giurgiulesti port handles over 70% of the Republic of Moldova's naval trade and is its only port with access to the sea, being positioned at the intersection of the Danube, the EU space and the Black Sea area. Through this move, our country consolidates its position as a regional hub and creates a major logistical advantage in a tense geopolitical context, in which trade routes and supply chains become instruments of power. The plans announced by the Government go beyond the simple takeover: investments to increase capacity, modernize infrastructure and integrate the port into an extended logistics system, connected to the Port of Constanta. Basically, an economic corridor is being created that connects the Danube to the Black Sea and, implicitly, to global markets, with Romania in a central position. The transaction also has an obvious geopolitical dimension: strengthening the relationship with the Republic of Moldova and creating an essential logistics platform for the reconstruction of Ukraine, given that the ports in the region have become critical infrastructure.