Episode 5 documented the transformation of BRICS+ into an alternative financial bloc through the creation of the New Development Bank (NDB). This sixth episode goes deeper, analyzing the technical mechanism through which financial autonomy becomes operational in 2026: BRICS Bridge, the payments infrastructure based on central bank digital currencies (mCBDC).

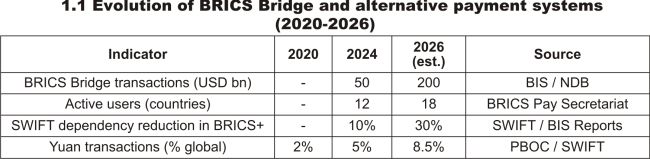

BRICS Bridge is not a theoretical concept - it is an active infrastructure that confirms a transformative reality: international payments without the dollar and without SWIFT are no longer marginal. They are an operational alternative that permanently fragments the global financial system.

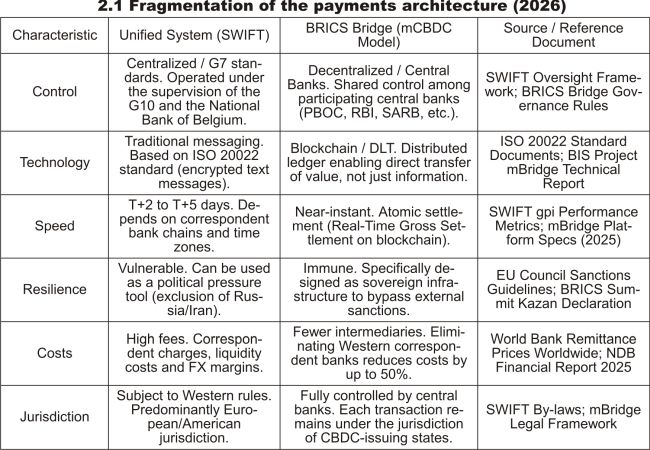

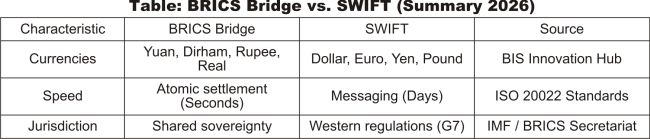

• 1. How BRICS Bridge works: Technical architecture

The objective is not the creation of a common currency, but the interconnection of national systems through CBDCs (Central Bank Digital Currencies).

- Interoperability: Systems are connected through permissioned DLT (Distributed Ledger Technology) technical protocols that allow direct conversion (e.g., Real to Yuan) without passing through the dollar.

- Role of blockchain technology: DLT is used to synchronize ledgers, enabling "atomic” settlement (simultaneous payment and delivery), without harmonizing national rules.

• 2. Managing imbalances and the cost of capital

A central issue is the accumulation of currencies that are difficult to reuse (e.g., excess rupees held by Chinese exporters).

- Currency swaps: Swap lines between central banks and accumulation caps are used to manage liquidity.

- Economic impact: The cost of capital becomes infrastructure-dependent. In 2026, money is no longer perfectly substitutable; an amount within BRICS Bridge has a different "velocity” and rules compared to one within SWIFT.

• 3. The need for an infrastructural alternative

The limitations of the NDB in its early years demonstrated that an institutional alternative is incomplete without an infrastructural one. In 2026, we have parallel infrastructures: SWIFT (dominant), CIPS (China), SPFS (Russia), and BRICS Bridge.

• 4. Implications for Romania

Opportunities:

- Payment diversification: Romanian companies exporting to India, Indonesia, or the UAE can use these nodes for faster settlements.

- Capital from the East: Facilitating energy transactions with Gulf partners (UAE, Saudi Arabia) that use mCBDC.

Risks:

- Secondary sanctions: Any settlement through BRICS Bridge with fully sanctioned states (Russia, Iran) may lead to the exclusion of Romanian banks from the Euro/SWIFT system.

- Volatility: Exchange-rate risk for Asian local currencies remains high.

• 5. Case study: MOL Group (Hungary) - Adapting to fragmentation

- Context: MOL Group, a regional giant also active in Romania, had to secure energy supply under SWIFT restrictions applied to Eastern suppliers after 2022.

- Solution: MOL diversified supply sources (Azerbaijan, Gulf region) and used alternative systems for local-currency payments (Dirham, Yuan) through banks in BRICS+ member states such as the United Arab Emirates.

- Result: A 12% reduction in transfer costs and maintenance of regional energy stability, while its subsidiaries (including those in Romania) accelerated renewable investments to balance eastern exposure risks. (Source: MOL Group Annual Report 2025)

• 6. Practical recommendations

- For investors: Track energy and agriculture companies that have the technical capability to operate in both payment systems.

- For Romanian firms: Prepare ERP systems to accept mCBDC digital payments, especially for relations with Asia and the Middle East.

• For policymakers: Monitor interoperability between the future Digital Euro and BRICS Bridge to avoid isolating Romanian firms from emerging markets.

BRICS Bridge is no longer a promise, but the reality that has ended SWIFT's monopoly. For Romania, economic success depends on the ability to function as a "translator” between these two financial worlds, maintaining integrity within the Western system while accessing Global South liquidity.